Saving, Investing and Inflation

Saving: The primary objective of is to “Safe” money.

Ex: Setting aside a portion of income in Piggy Bank.

Investing: The primary objective of is to “Earn Profit”.

Ex: Investing in Mutual Funds, Stocks, Bonds and Golds etc.

Inflation: The rate at which rises, Eats up your savings over time.

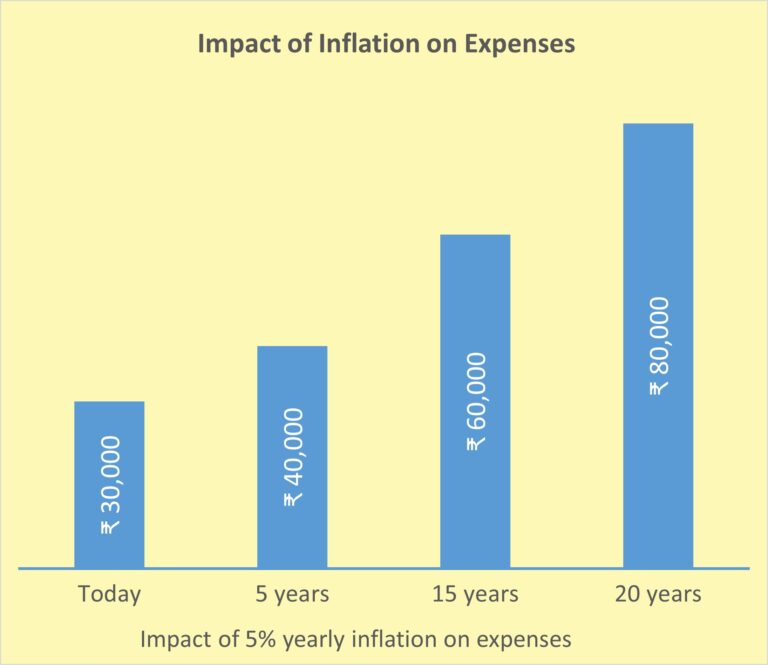

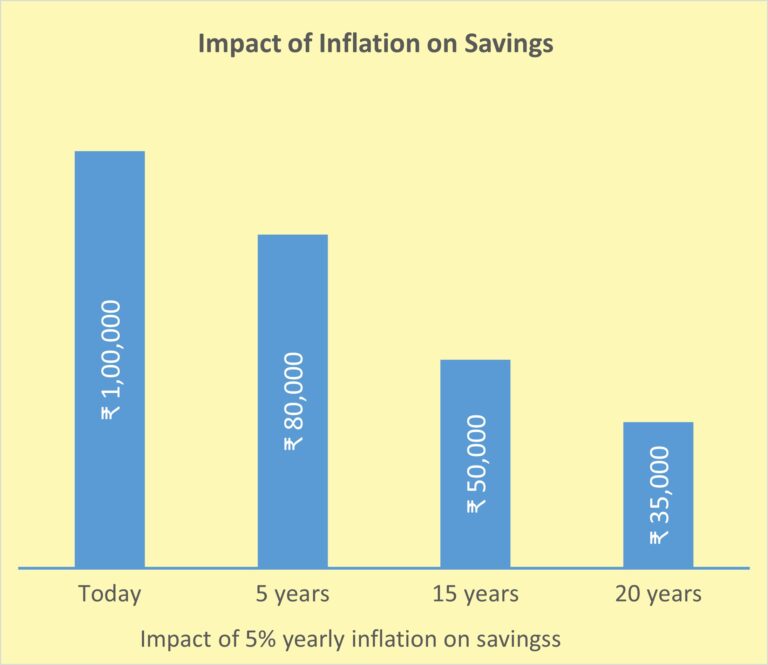

Impact of Inflation

Disclaimer: For illustration purpose only | Assumed rate of inflation as 5%

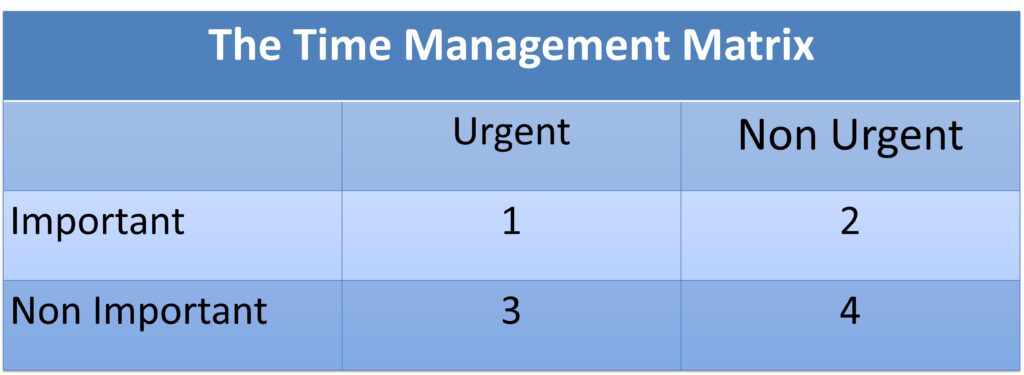

Why should one invest ?

Stephen Covey discussed in his bestseller “The Seven Habits of Highly Effective People”

In the book, Covey says that as long as you keep focusing on Quadrant I, it keeps getting bigger and bigger and then starts to dominate you. This quadrant referred to by Covey is “urgent and important”. When that happens, the ‘important but not-so-urgent’ tasks are not planned for in time until they also enter the quadrant 1, becoming urgent. The same principle applies to financial goals, too. A large number of people struggle with their finances since they do not plan for the important and not urgent events in life.

Wisdom suggests that if one plans well for those important and not urgent tasks (and goals), life changes for the better. In order to achieve this, it is important to first classify the financial goals – those events in life in terms of timeline and importance in one’s life.

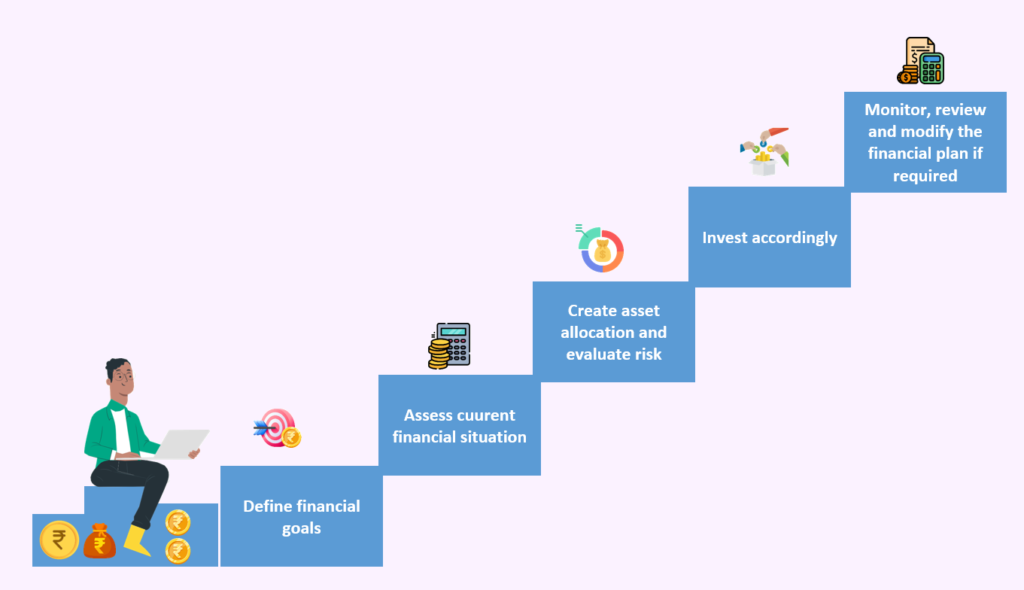

What is Financial Planning ?

Financial Planning is the practice of assessing one’s current financial situation and drawing a financial plan to reach future life-stage goals.

Steps of financial planning

Real Estate Traits

Location is most important

It is not a divisible asset

Real estate is Non-Transparent

Physical and financial form

Capital appreciation and current income

Transaction cost is very high

Maintenance cost must be adjusted before calculating returns

Make your investments work for you

Your Investment should

Provide income when you need it

Be accessible & usable in parts and portions

Grow in value and appreciate over time

Be realizable at fair value and low cost

Through proper Asset allocation we can achieve these goals.

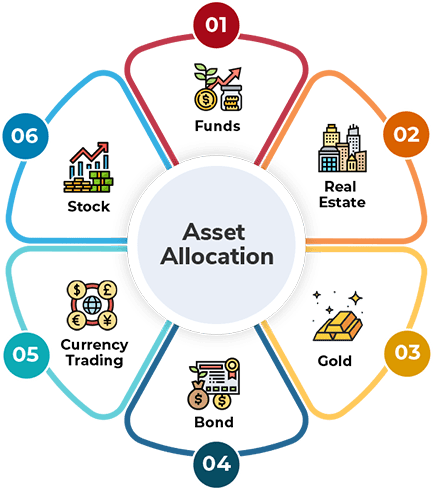

What is Asset Allocation ?

Factors to evaluate Investments

Investment Risks

Market rise and Price risk

Mutual Fund Industry Size of India

Average Assets Under Management(AUUM) of Feb 2026

₹ 83,42,616.57 crore (83.4 trillion)

Total no. of Accounts as on Feb 2026

27.05 crore

SIP inflows in Feb 2026

₹ 29,845 crore

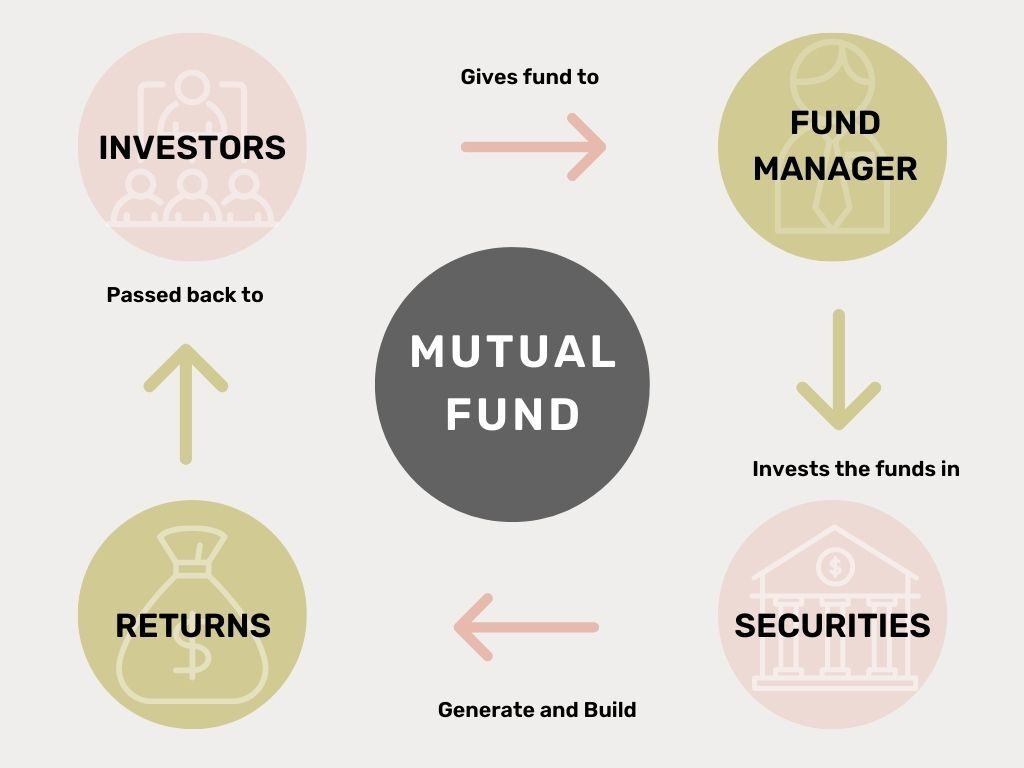

What is Mutual Fund ?

A mutual fund is a financial vehicle (scheme) that collects money from many investors and invests it in securities such as stocks, bonds, debentures etc by Fund Managers and gives better return in long term.

Advantage of investment in Mutual Funds

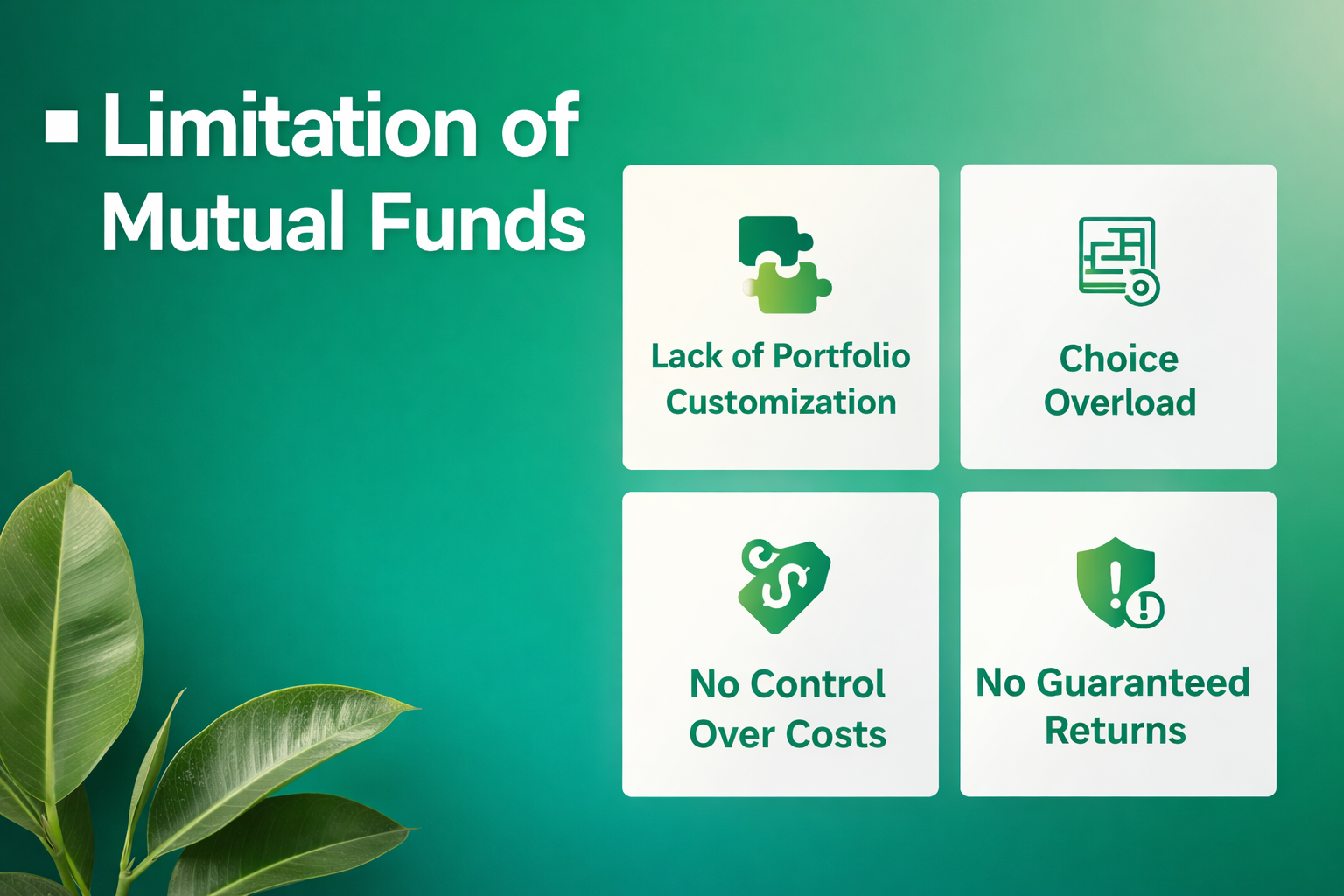

Limitation of investment in Mutual Funds

Organizational Structure of Mutual Funds in India

Basic Terms & Concepts in Mutual Funds

Asset Management Company (AMC)

An Asset Management Company (AMC) is a financial institution that manages investments on behalf of individuals and institutions. It pools money from many investors and invests it in various assets like stocks, bonds, and other securities to generate returns.

Assets Under Management (AUM)

Assets Under Management (AUM) refers to the total market value of all investments that a financial institution manages on behalf of its clients.

Net Asset Value (NAV)

Net Asset Value (NAV) is the per-unit price of a mutual fund. It tells you how much one unit of a fund is worth on a given day.

NFO (New Fund Offer)

NFO (New Fund Offer)is the first-time subscription offer of a new mutual fund scheme launched by an Asset Management Company (AMC).

Portfolio

A Portfolio is a collection of all your investments in one place.

XIRR (Extended Internal Rate of Return)

XIRR (Extended Internal Rate of Return) is a method used to calculate the actual annual return on investments when cash flows happen at irregular intervals. XIRR tells you your real return when you invest and withdraw money at different times (like SIPs, lump sums, redemptions).

Growth Option

Growth Option in a mutual fund means that the profits earned by the fund are not paid out to investors, but instead are reinvested back into the fund.

Dividend or IDCW Option

Dividend Option (now called IDCW – Income Distribution cum Capital Withdrawal) is a mutual fund option where the fund pays out a part of its profits to investors periodically.

Lump Sum Investment

Lump Sum Investment means investing a large amount of money at one time instead of spreading it over a period.

SIP (Systematic Investment Plan)

SIP (Systematic Investment Plan) is a way of investing in mutual funds where you invest a fixed amount regularly (monthly/weekly) instead of investing a lump sum.

STP (Systematic Transfer Plan)

STP (Systematic Transfer Plan) is a mutual fund strategy where you transfer a fixed amount regularly from one fund to another, usually within the same Asset Management Company (AMC).

SWP (Systematic Withdrawal Plan)

SWP (Systematic Withdrawal Plan) is a mutual fund facility that allows you to withdraw a fixed amount regularly from your investment.

Switch

Switch (in Mutual Funds) means moving your investment from one scheme to another within the same Asset Management Company (AMC).

Expense Ratio

Expense Ratio is the annual fee charged by a mutual fund to manage your investment. It covers fund management, administration, marketing, and other operational costs.

Exit Load

Exit Load is a fee charged by a mutual fund when you redeem (withdraw) your investment before a specified period.

Direct Plans

Direct Plans in mutual funds are schemes where you invest directly with the Asset Management Company (AMC) without involving any broker, agent, or distributor.

Regular Plans

Regular Plans in mutual funds are schemes where you invest through a broker, agent, or financial advisor, instead of investing directly with the AMC.

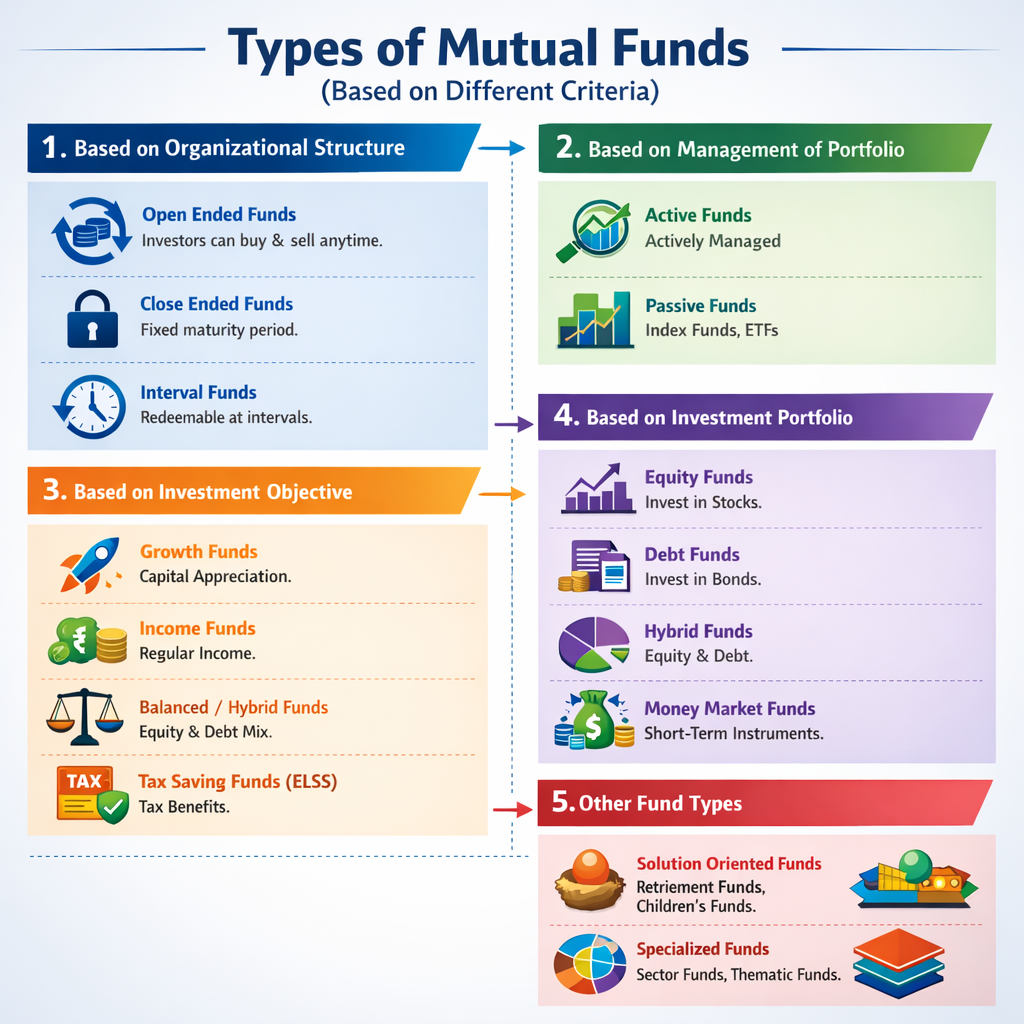

Categorization of Mutual Fund Schemes

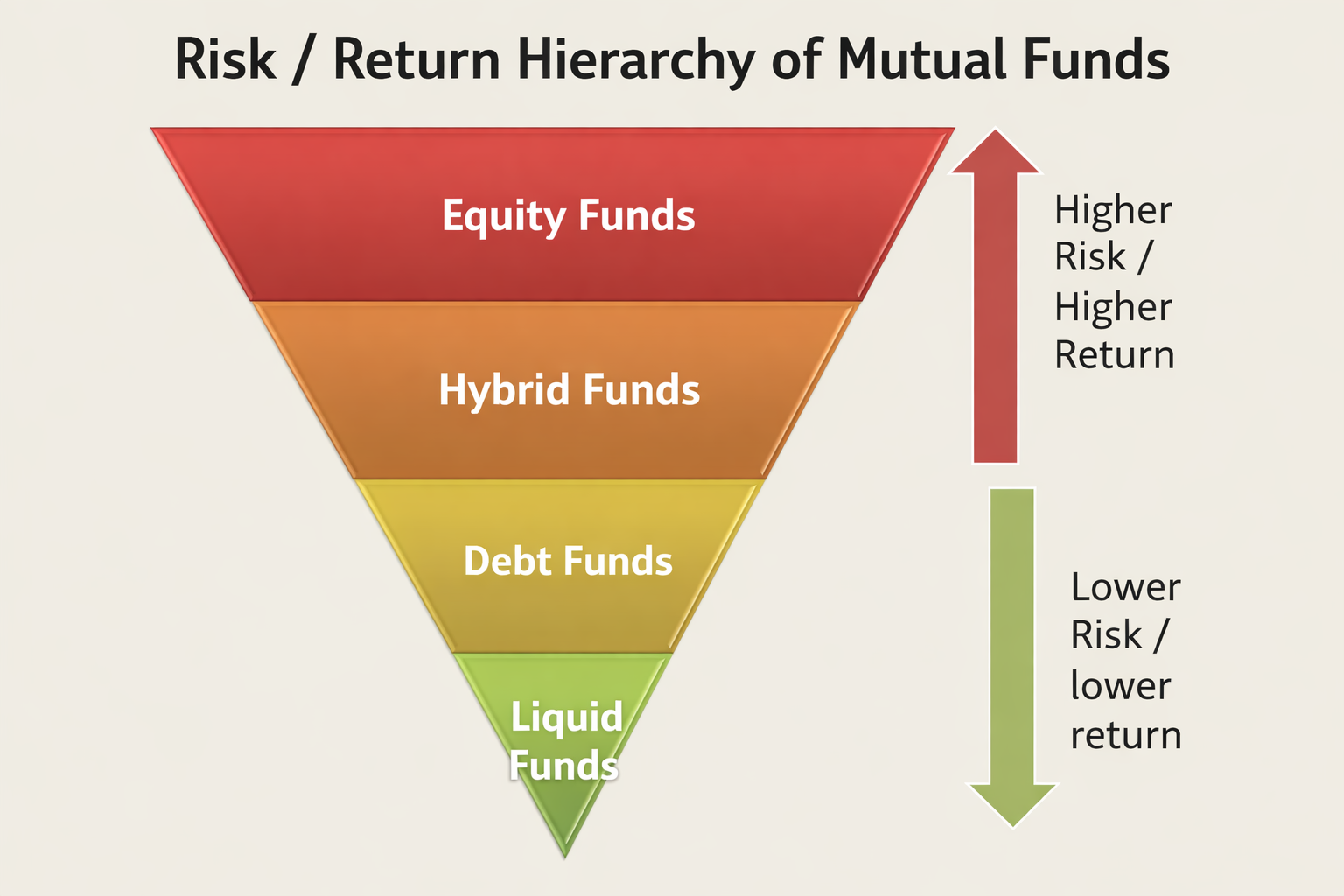

Risk / Return Hierarchy of Mutual Funds

Equity Funds

- Invest in equities and equity related instruments of companies

- Seek growth in the long term, can be volatile in the short term

- Suitable for investors with higher risk appetite and longer investment horizon

Equity Fund Categories

Multi Cap Fund

At least 75% investment in equity & equity related instruments. Also referred to as Diversified Equity Funds. Minimum 25% in Large , Mid and Small Cap.

Large Cap Fund

At least 80% investment in equity & equity related instruments

Large & Mid Cap Fund

At least 35% investment in large cap stocks and 35% in mid cap stocks

Mid Cap Fund

At least 65% investment in mid cap stocks

Small cap Fund

At least 65% investment in small cap stocks.

Flexi Cap Fund

An open ended dynamic equity scheme investing across large cap, mid cap, small cap stocks

Dividend Yield Fund

Predominantly invest in dividend yielding stocks, with at least 65% in stocks

Value Fund

Value investment strategy, with at least 65% in stocks.

Contra Fund

Scheme follows contrarian investment strategy with at least 65% in stocks

Focused Fund

Focused on the number of stocks (maximum 30) with at least 65% in equity & equity related instruments.

Sectoral/ Thematic Fund

At least 80% investment in stocks of a particular sector/ theme

Equity Linked Savings Scheme (ELSS)

At least 80% in stocks in accordance with Equity Linked Saving Scheme, 2005. Deduction from taxable income of up to Rs.1,50,000 under Sec 80C. Shortest lock-in period of 3 years

")

")